Every employer should have access to an Employee Benefits Platform (EBP).

The technology is proven and has been in use for well over a decade, both globally, in multinational firms, and in large UK corporates.

Slowly, it has also been making progress in mid-market businesses with more than 100 employees, but it is still relatively rare to see an EBP in place for small businesses. Why is this?

Technology is not the barrier

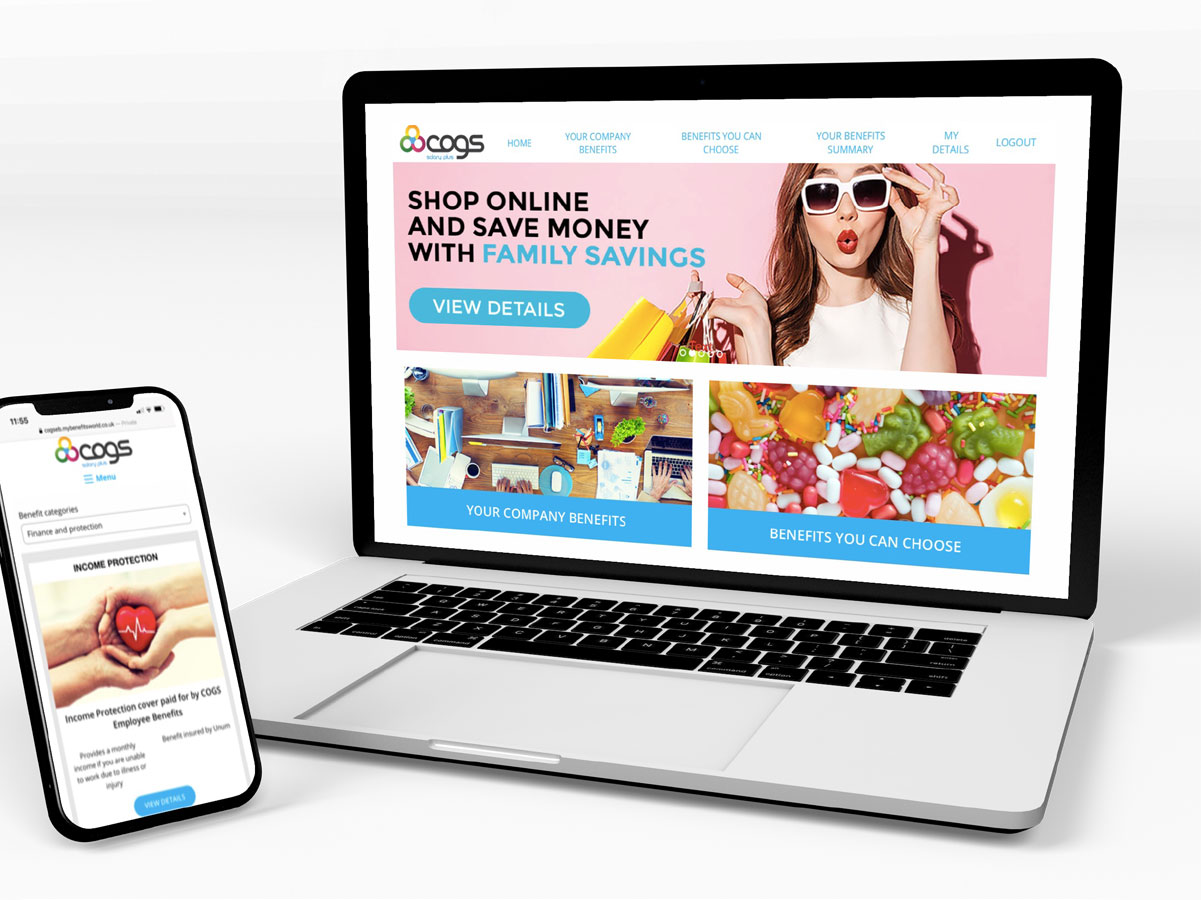

Most EBP’s are simply websites that are hosted in the cloud.

The main functionality is a relatively simple selection tool that allows you to pick certain services – not much different than any retail website that a shop would use.

There is a reporting suite of varying levels of intensity but nothing too complex stands out here.

Why are Employee Benefits Platforms so expensive?

If most small businesses can afford to have a retail website to sell their products, why on earth are EBPs so expensive when the technology is so similar? It is clearly not the cost of the technology.

Two clear trends have given rise to the historical high cost of an EBP

1. Lack of competition

Anyone familiar with the employee benefits market knows that there are two large global players who dominate the market.

Without competition, these dominant forces can effectively charge what they like for their services (to a point).

New entrants seeking to disrupt the market with a streamlined proposition, offer more affordable options to UK clients. This competition from market disrupters like Employee Benefits Collective has forced down the cost of an EBP for UK employers.

2. Excessive people costs

Traditional EBP providers have a vast array of people involved in its delivery:

- A ‘flexible benefits’ consultant

- a project manager

- an implementor / technology consultant

- a platform administrator / helpdesk operator

- a platform developer

- a communications specialist

- a pension consultant, and

- a benefits consultant.

With a typical salary of somewhere between £20,000 - £100,000, depending on experience, the underlying wage bill when offering an EBP can be significant.

However, are this many people required to offer this service?

How much of their cost should be met by the EBP pricing?

Are there areas that could be automated or processes that could be simplified to remove some of these costs?

Again, many new providers in the market (such as EBC) have:

- up to date technology that helps makes running an EBP much easier

- streamlined processes and approaches that limit the need for all these people

- dramatically reduced the underlying cost of setting up and running an EBP

An Employee Benefits Platform for all

By offering an alternative approach and keeping things simple / modular, you can offer an EBP that can be affordable to any type of business in the UK including SMEs.

However, EBPs are just a front end for your employee benefits.

More trends

A revolution is slowly, but consistently, occurring in the delivery of individual benefits as well.

We can see this across several areas:

The most obvious example is online quotations for many major employee benefits. However, there has also been a surge in useful marketing material including social media integration, adverts, and video content that can be distributed to clients.

Online membership databases is a good example of the progress here.

Online support includes accessing documentation through to completing renewals online.

Employee friendly websites and apps can allow an employee to access their documentation and make a claim online. Some benefits are entirely delivered online – like Virtual Private GP services.

Using the 2/3rds guide

The Future is Bright

They say that it is only after the first 10 years of a technological innovation that you start to see the difference that it makes to how you work or live.

I’d maybe change that for the employee benefits industry to 20 years, but there is no doubt that technology is finally making its impact felt through platforms, apps and online administration with plenty more to come in this space.

Andrew